There are some people who may ask the question who is in charge of filing form 1099? And do I even need one? We’ll get into the variety of 1099’s in this article and what the purposes of filing these IRS forms are for.

How to file form 1099 isn’t rocket science but you need to know the type of income you’re making to learn whether getting into this IRS form is ideal for you. Or do you need another type of IRS form yourself?

What is an IRS 1099 Form?

A 1099 form is a record of an organization or person gave you money. In the case of 1099-MISC it is specifically money which is not gained through usual employment routes. The payer fills out the 1099 form and send you copies and the IRS.

What are the uses of form 1099?

1099’s help a tax payer figure out how much income is received during the year and the kind of income it is. You’ll report that income in different places on your tax returns.

Who should get a 1099 form?

All people, tax payers can get a 1099 form. Freelancers and independent contractors can get a 1099-MISC or 1099-NEC from their clients.

These forms usually reflect the money which clients pay the freelancer or independent contractor.

Normally, 1099’s have your SSN or Social Security Number and TIN or tax identification number.

This means the IRS knows you received money and it will also know if you don’t report it on your tax return.

Is Form 1099 the same as Form W-2?

The phrase 1099 employee usually means a person who is working as an independent contractor or self employed.

So 1099’s are not the same as W-2’s which report income paid to employees. If you get a 1099 from your employer, this usually means you are seen as an independent contractor.

Types of 1099 Forms

1099-A

You can get this if you’re a mortgage lender and you were involved in a short selling period of your home. If you canceled some of your mortgage, then it’s taxable.

1099-B

This is income which includes the sale of several types of securities. You may also have used this through bartering exchanges and websites.

1099-C

If you have asked a credit card company to lower your debt, the amount the lender forgives may be taxable. Hence 1099-C.

1099-CAP

You can get this form if you hold shares of a corporation which was acquired or had changes in it’s capital structure. If you got cash or property as a result of those changes, you are likely to get into 1099-CAP.

1099-DIV

This is a really common form of 1099. It reports dividends which you get including those you get from a credit union. IRS thinks of those as interest hence they could also appear on 1099-INT.

1099-G

If you received money from the state, local or federal government, including a tax refund, credit or offset, you may get this form. If you’ve had unemployment during the year, you may have a 1099-G coming your way.

1099-INT

If you earn more than $10 interest in a bank or other financial institution, you may receive a 1099 INT.

1099-K

Freelancer and small business owners if you have received $600 worth of business income from a client through a credit card or a third party payment system.

1099-MISC

This form is for other income which won’t fit into the other categories. Income from prizes and awards are also used here.

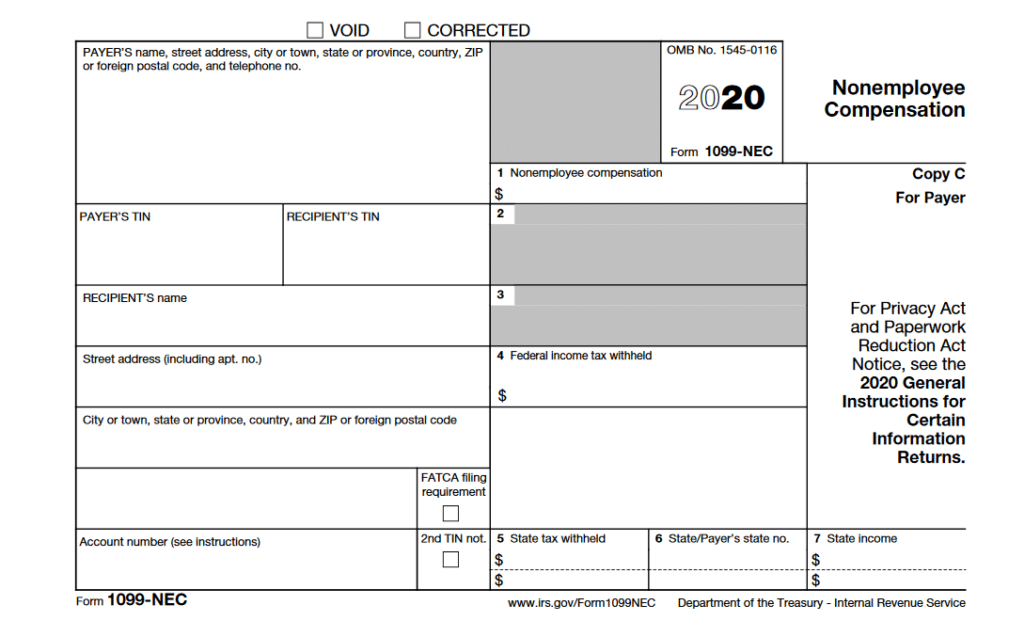

1099-NEC

This is a recent form for people who received income but were not employees. If it is a freelancer or a gig, then you ought to get Form 1099-NEC.

1099-PATR

1099-PATR is for those who are into co-ops and receive at least $10 in patronage dividends.

1099-Q

This is for people who save a decent 529 account for college tuition. This means that the 1099-Q is for reporting money that you and your child receive from the 529 plan.

Take note though that funds you receive through 529 are not taxable and more often than not, this is just for record keeping.

1099-R

Income from a pension, retirement plan, IRA or annuity and profit-sharing come from this form. If you take a loan from your retirement plan it can be considered a distribution.

1099-S

People responsible for closing sales on real estate typically show these to you and report the proceeds. Again, sales from a house are not necessarily taxable, so it’s important to check with your state’s laws and statutes.

HOW TO FILE A 1099 FORM

1. If you’re an independent contractor, get 2 copies of 1099’s from your client.

One copy is for your records, while the other copy is for the IRS. You need to keep your own copy in case the 1099 is ever lost or damaged.

2. Proof-read your 1099’s.

The IRS will automatically match up the 1099’s that they receive with the ones that you submitted to any of your clients. If they see a discrepancy, then they will send out an audit notice.

3. Organize your 1099’s Per Year, and Per Category

Since it can be difficult to sort through all of your 1099’s, it’s best to organize them by year, but also by type. So if you have 1099’s from different plumbers and electricians, then it helps if you organize them separately. This way when tax time comes around, you won’t have any issues sorting through them quickly.

4. Keep track of your income so you don’t overpay taxes.

When using your 1099’s for tax time, be sure to keep track of how much money each one makes every year so that you’re not overpaying taxes.

One of the best ways to track your income is through the use of an online pay stub generator.

5. Show up on time.

Show up on time. If you’ve been keeping track of your gross pay and your net pay, you’ll be on top of taxes come tax season. So it’s a good idea to show up early and get it over with when it’s time to do the filing.

6. Write off your personal expenses.

Write off all your personal expenses, because this helps the tally in showing that you really were running a business and that whatever it is you do cannot be considered just a hobby.

7. Writing off mileage and car expenses.

If you’re self-employed, there may be times when you have to use your car for business. Mileage is probably the biggest deduction, but a percentage of the wear and tear on your vehicle from business use can also be deducted in one of two ways.

The first is to take a mileage deduction for the actual miles driven on business.

You will either need to keep a log of your trips or you can use software that tracks your mileage automatically. However, this option generally only works if you have a certain amount of miles per year.

The second way that you can deduct the wear and tear on your vehicle is by using the standard mileage rate.

This is currently 18 cents per mile and it was 20 cents before 2017. There are also some limitations in terms of what type of vehicle you can use this deduction with, but if your car qualifies then this is probably going to be the better option for most people.

If you’re going to go with the standard mileage rate, then it’s best to do so for the entire year at once and all in one shot. This will help reduce any issues with what kind of expenses can be deducted and how much you’re allowed to deduct since it will be compiled together from the start.

8. Maximize tax deductions for a house and rent.

When it comes time to file taxes as a homeowner, don’t forget about all of the costs that go into keeping up your home. While there are many possible deductions, these are likely some of the biggest ones:

There are two ways that eligible taxpayers can calculate the home-office deduction. In the simplified version, you can take $5 per square foot of your home office up to 300 square feet,

If the home office is not your principal place of business, you can also take a regular deduction. This is calculated by taking the square footage of the office divided by 9 and then multiplied by $5.

If you rent out part of your home, you can deduct between $25 and $100 per month for each room, depending on how big it is. If it’s just a den or a bathroom, then the limit is $25. If it’s a large bedroom or living room, then you can deduct up to $100 per month.

9. Deducting work-related education expenses

If you have to go back to school because your job requires new skills, then you may be able to deduct some of those costs this year. However, it’s important to note that only education costs that are related to maintaining or improving job skills can be deducted as an employee expense.

10. Outsource your Payroll if you’re having a hard time.

If you’re making enough passive income and it appears that you cannot get enough time every tax season or payroll period if you have a number of employees? Then maybe it’s time to Outsource.

You can Outsource your Accounting and Bookkeeping tasks or any number of administrative routines you have as long as you find the right Remote Staffing company.